Market Update - March 2024

/The spring market in Denver is off to a great start. It seems that sellers are taking the prospect of interest rate cuts to heart and starting to list their homes in spite of the “rate lock” effect. New listings increased 16.27% above February 2024 but they were still down about 3.28% from March of last year.

You may have heard rumblings about the NAR ruling, if you’d like to read our thoughts and opinions on the settlement and its consequences check out our blog post on the topic.

Will Rates Fall?

The big question is if there will actually be 3 rate cuts in 2024. Job growth has been really strong, data from the Bureau of Labor Statistics (BLS) showed that February marked the 38th consecutive month of job growth in our economy, which is the fifth longest period of employment expansion in the history of our economy and the longest stretch of unemployment figures below 4% in over 50 years.

After the jobs report came out Jerome Powell stated that there would be no interest rate cuts in March, and in the days following the Federal Reserve meeting two other members of the Fed board came out and stated that they are not sure if inflation and job numbers will support any rate cuts at all this year.

Obviously markets reacted to that news and the stock market had the worst week it’s had in a year. Investors are anxious that the Fed will not actually cut rates in 2024 which could lead to some pain for large corporations who will eventually be forced to refinance their debt.

Whether or not there will be rate cuts depends heavily on inflation trends and the jobs reports that the BLS puts out. The US Federal Trade Commission also recommended that Congress scrutinize grocery profits as the FTC released a report that found that large market participants like Kroger accelerated and distorted the negative effects of the pandemic to increase profit, also known as price gouging, which they absolutely did all over the country.

I bring this up because grocery prices are part of the inflation calculation and simply cutting interest rates with no congressional oversight into corporate price gouging likely won’t solve the inflation problem. How is it $8.50 for a bottle of Cholula at the grocery store? Price gouging! Check out Kroger’s stock price, it was about $29 a share before the pandemic and today it’s at $55.32 which is way outpacing inflation.

Source: Yahoo Finance

Crazy, right? That’s probably enough waxing philosophical on the economy for now.

Market Anecdotes

In March we saw a flurry of market activity in spite of intense weather, spring break, and Easter, all of which normally contribute to some sleepiness in the market. We had high open house traffic, even on Easter weekend.

We also saw competition at all price points below $2M for properties that are nicely updated and priced well. Dated properties or properties that are overpriced continue to sit on the market longer which is driving up average days on market. The competition for properties priced between $500k - $750k can be very intense as this is the most active segment of the market from a pending and closed listings perspective.

Buyers tend to have high expectations of properties because the cost of borrowing is so high. We’re seeing a lot of pushback on properties that were updated in the early 2000s - buyers think these updates look dated now while many sellers think a kitchen remodel done in 2004 is still chic and fresh despite being 20 years old. Warm color palettes with beiges, skinny horizontal glass tile backsplashes, and tuscan style tile work and cabinetry are all turnoffs for buyers looking for updated move-in ready homes.

The Stats

The number of pending listings is often used as an indicator for buyer demand. In March 2024 pending listings were at the highest level they’ve been since August 2022 when interest rates first started increasing. This is indicative of an uptick in buyer activity and a resilient and fast-paced market.

3,106 pending listings in March 2024 and 3,178 pending listings in August 2022.

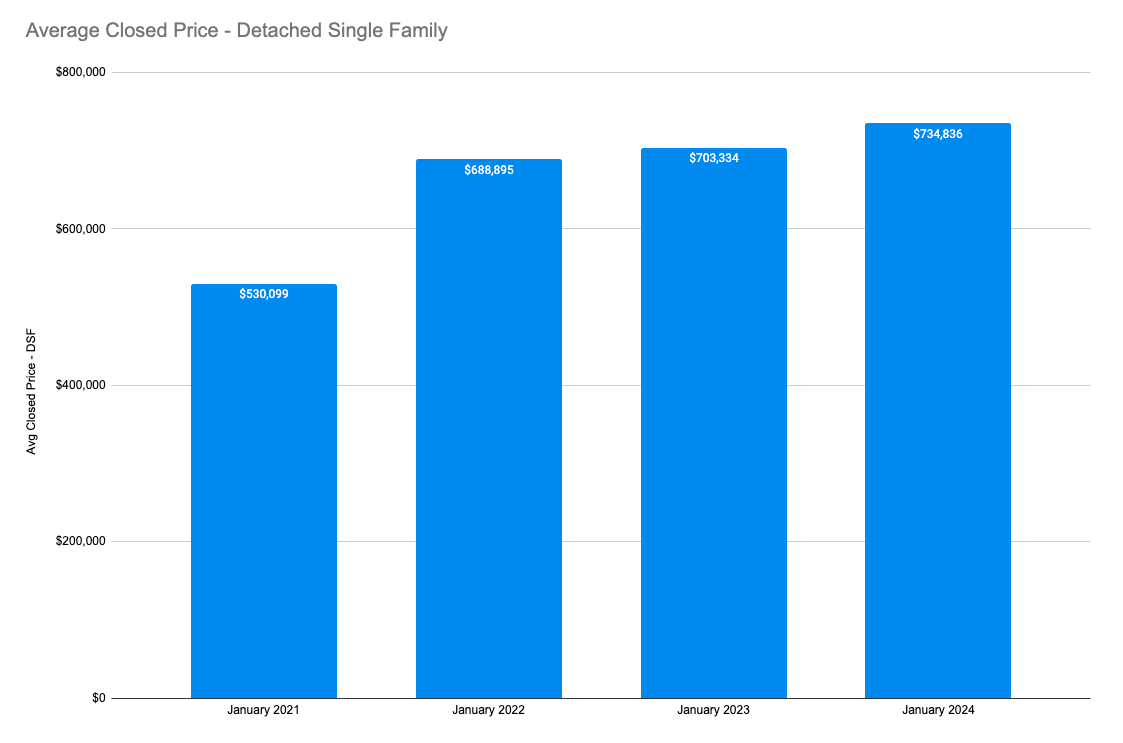

Average Closed Price

Average Closed Price for Detached Single Family homes was $776,919 which is a 4.34% increase Year-over-Year (YoY) and a 3.19% increase from February 2024.

Average Days on Market

Average Days on Market (DOM) was flat YoY at 39 which is a huge increase from 2021 and 2022 numbers, but has been around this level since interest rates increased.

Local Topics

Denver approved a blanket rezoning of the Hale Neighborhood to allow for Accessory Dwelling Units (ADUs) to be built which eliminates the need for a homeowner to apply to rezone their property in order to build an ADU. More and more neighborhoods in Denver keep changing these zoning regulations to respond to the need for more housing in the city.

The Colorado state legislature approved Senate Bill 94 which will require landlords to finish serious repairs within 7 days and less serious issues within 14 days. The bill aims to close a bunch of loopholes in the Warrant of Habitability Law from 2008 and is headed to Governor Polis’s desk for review.

The City of Denver released a budget plan showing exactly how the city plans to fund programs for new migrant arrivals through the end of 2024. They have already spent $25M of the $90M plan with the bulk of the funds going to Shelter & Housing. You can check out a breakdown of the budget here.